A Receiver’s Guide to Investment Strategies

A receiver has a duty to prudently invest funds of the estate, but this task is often complicated and nuanced. When distributions to claimants are delayed for many years, the receiver’s decision of where and how to invest is crucial. The opportunity cost of maintaining large sums in low-interest accounts can be significant. Receivers must consider the trade-off between the potential for higher yields and the necessity for liquidity to cover immediate estate expenses.

Here are some options that receivers should consider as they develop an investment strategy:

- FDIC-insured bank accounts at multiple banks

- Insured Cash Sweep Account (ICS)

- Special Balance Account

- Qualified Settlement Fund Account

- Systematic Important Bank Account (SIB)

- Bank Accounts - Surety Bonds

- Certificates of Deposit (CDAR)

- Treasury Securities

If the total amount of receivership funds is in the hundreds of millions, banks might have limits on how much receivers can deposit. For example, withICS accounts, the limit is typically $150 million, but it is best to check with your banker because some banks will go higher, and others have lower limits.

Banks provide essential services, such as website and claims management, which are often included as benefits. They may also waive fees for wire transfers and offer simplified payment and distribution processes. Keeping funds in a bank account offers daily liquidity, and in all cases, receiverships need to have bank accounts to administer estate funds. But bank account interest rates are subject to market fluctuations, and having all funds in floating rates introduces interest rate risk, even if rates seem attractive today.

While not generally providing interest as high as Treasury securities, certain banks can get very close depending on the anticipated deposit term. Some banks, like Axos, offer bank accounts where the funds are fully protected (ICS), along with the case administration benefits mentioned above. Banks that offer these rates of return and included services should also be considered a viable option to balance liquidity needs and interest.

Treasury securities typically offer the highest yield. Their shortest maturity is four weeks, and Treasuries can be purchased by opening an account on treasurydirect.gov, opening a brokerage account, investing in a money market fund that holds exclusively Treasuries, or investing in a higher yield money market fund that includes Treasuries and other types of highly rated short-term investments. A money market fund provides next-day liquidity and is considered one of the safest investments. It has dipped below the target share value of $1 (known as “breaking the buck”) during a few volatile markets or due to changes in inflation and interest rates but has quickly recovered.

Maturity Diversification

If funds are expected to be distributed over longer periods, maturity diversification becomes a key strategy for prudent investing. It mitigates interest rate risk and reduces operational challenges associated with short-term investments. If substantial funds are expected to be held for five years, for instance, investing in a five-year Treasury may be wise if the receivership order gives a receiver the flexibility to buy longer-term securities. This strategy protects against interest rate volatility by aligning the investment duration with the anticipated cash outflow. The strategy presents minimal operational issues because Treasuries are highly liquid. If the funds are needed sooner, they can easily be sold.

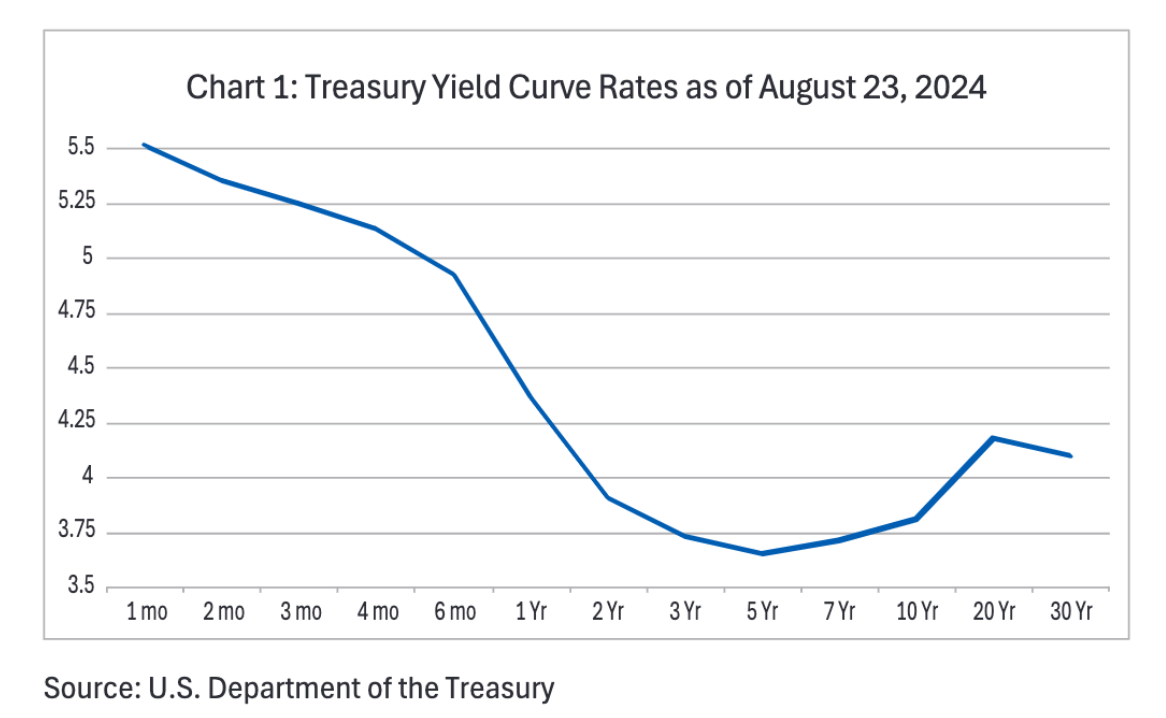

On the other hand, if funds are not needed for months, investing in a layered strategy of Treasuries with different short-term maturities may be the most prudent strategy. See Chart below for the treasury yield curve.

However, investing and rolling over the proceeds when they mature involves a larger time commitment than keeping funds in a bank account. As a result, for receiverships with smaller cash reserves, the time spent on it would not make economic sense. Investing in a short-term bond fund focused on Treasuries could reduce time spent on management. However, compared to directly purchasing Treasuries, a bond fund is more susceptible to market fluctuations due to interest rate changes. Treasury bond prices at maturity are fixed, whereas bond fund values can vary.

In short, receivers need to consider the benefits of both bank accounts and Treasuries, the expected duration of the receivership, and their fiduciary duty to maximize potential returns for claimants when determining how much to place on deposit and to invest.

What Happens When the Estate Accumulates Money?

It is not uncommon for receiverships to accumulate millions of dollars on behalf of defrauded investors and other claimants. Depending on the complexity of the case and the number of victims, it might take years before distributions are made. In the interim, claimants may contact receivers for case updates and inquire about when they should expect payment, while others will depend on updates posted on the receivership websites. The claimants might also seek to understand how the funds are invested and the returns the estate generates.

Furthermore, claimants can estimate the effective interest rate by reviewing the interest income entries in forms filed with the court, for example a Standardized Fund Accounting Report (“SFAR”), provided there has not been a significant change in the cash balances from one period to the next.

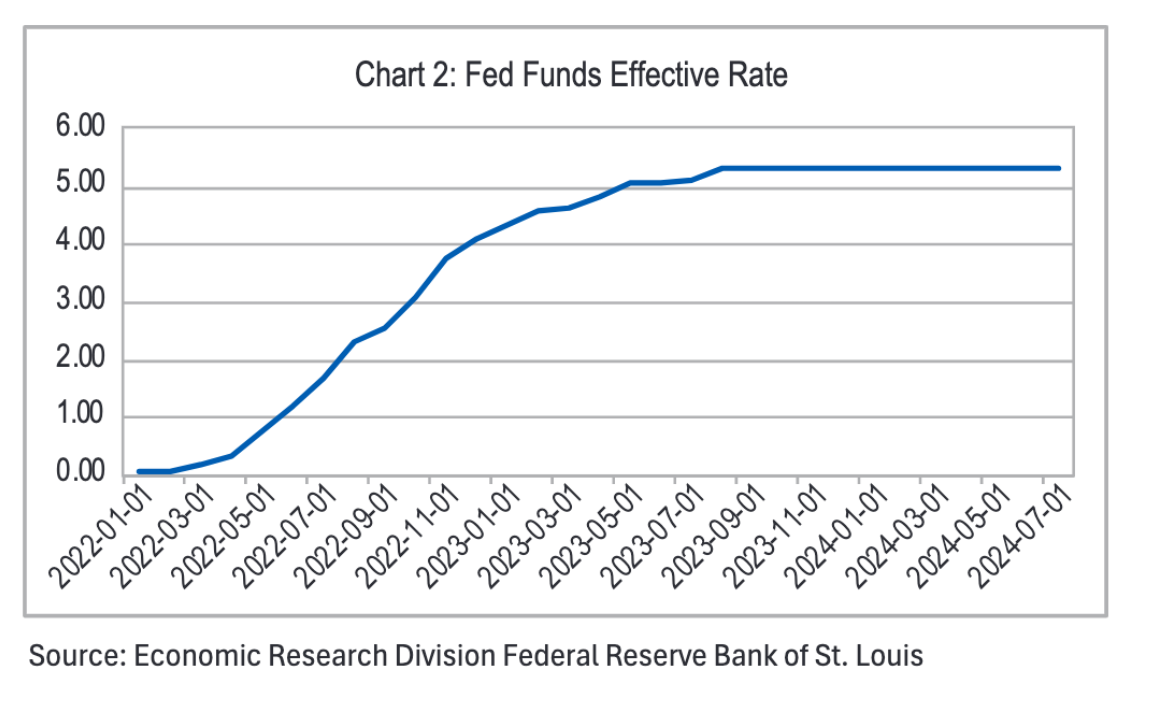

Since 2022, Federal Reserve officials have increased the central bank’s benchmark interest rate ten times consecutively to temper the U.S. economy and curb inflation. The Federal Reserve paused its rate-hiking campaign in July 2023. See Chart 2 below.

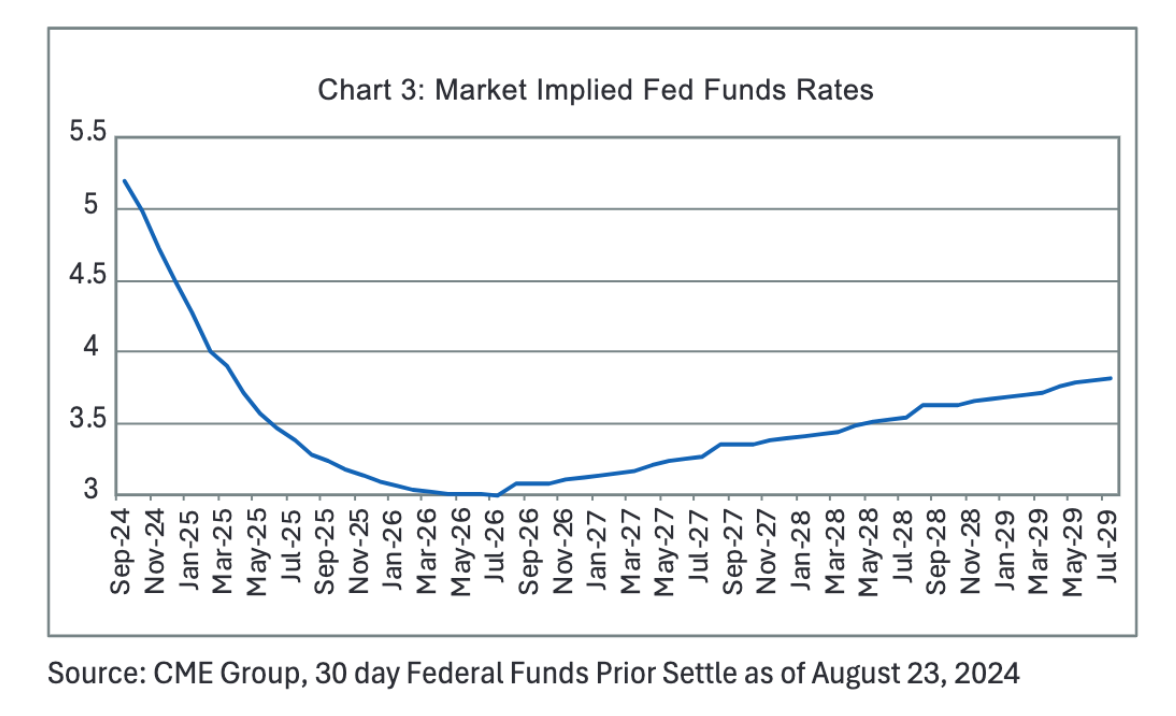

The Federal Reserve is expected to reduce rates starting in September 2024 because inflation has moderated. But rates are unlikely again to fall below inflation and return to the close to zero levels like we have seen in the past, and they might stay elevated. See Chart 3 below.

When interest rates were close to zero, investment income was minimal and rarely discussed. In recent months, however, the landscape has shifted due to a significant rise in interest rates. Investment income has emerged as a more significant source of increasing the estate’s recovery.

Should a claimant discover that the receivership estate’s effective interest rate on its investment income is significantly lower than current market rates or inflation, it is probable that the receiver will be contacted by a concerned claimant, particularly as the funds erode in purchasing power as time progresses.

Moreover, when interest returns are grossly short of the market standards, absent a good reason, the claimants’ concerns can swiftly escalate to ire, and they might decide to contact the judge overseeing the case. This situation not only tests the patience of claimants but also poses a direct risk to the receiver and could have implications for a receiver’s fee petitions.

The Receiver’s Duty to Invest Funds

Because the primary objective of the receiver is the preservation of the estate, in the words of Ralph Ewing Clark, “the law must guard those funds with great jealousy.” The receiver must manage the funds in accordance with the directions of the court. Any action beyond those expressly or impliedly provided by the court subjects the receiver to personal liability.

Although receivers and bankruptcy trustees both act as fiduciaries, they are appointed by different courts, with different rules governing their appointment and fiduciary responsibilities. Specifically, bankruptcy trustees are bound by the Federal Bankruptcy Code while federal equity receivers are bound by federal district court rules and court orders.

In bankruptcy, there are case opinions that opine on how trustees should manage investment income. These guidelines are useful for receivers to review because the practical considerations of both receivers and trustees are similar. In Matter of Accomazzo,a federal court in Arizona stated:

"[T]he practical considerations involved in defining a trustee’s duty to maximize the return on the bankruptcy estate’s funds are 1) the sum of funds subject to investment, 2) the duration of the trustee’s administration of the estate, 3) the time required by the trustee to manage the transfer of funds, and 4) the frequency with which a trustee needs to access those funds."

Although my research has not revealed any federal equity receiver being surcharged for lost interest, following the four practical considerations listed above is good advice for avoiding a judge’s inquiry of why investment income may be comparatively low. In the Accomazzo case, the bankruptcy trustee was found liable and was surcharged the interest the estate should have received because the trustee did not follow the practical considerations. “When the practical considerations weigh in favor of investing the funds, absent other compelling justifications, a trustee may be found negligent for failing to do so,” the court concluded.

The Model Receivership Order

Because a receiver has no power or discretion absent an express or implied order of the court, the receiver’s duty to invest is determined by the appointment order or pursuant to a receiver’s petition to the court for permission to invest. Receivers should have the benefit of being more flexible in their cash investments, especially because the time cash is held is often significantly longer than in bankruptcy. Sometimes the order is very limited and only allows the receiver to place funds in specific banks or in banks with a physical branch within the federal district of the appointing court, or to keep existing accounts open. Where feasible, a court order encompassing broad language that grants appropriate investment flexibility should be proposed, such as the following language:

Open one or more bank or securities accounts as designated depositories for funds of Defendants and Relief Defendant. The Receiver shall deposit all funds of Defendants and Relief Defendants (or related person within the meaning of Treas.Reg. §1.468B-1(d)(2)) in such designated accounts and shall make all payments and disbursements from the receivership estate from such accounts. The Receiver is authorized to invest receivership funds in U.S. Treasury securities, money market funds or other interest-bearing accounts as appropriate in the Receiver’s judgment.

Receiverships Are Not Subject to Bankruptcy Investment Rules

Fortunately, it is uncommon for receivership orders to include language in the order that the administration of the estate’s funds should be subject to the Money of Estates Act,11 U.S. Code § 345. The Money of Estates Act requires that all deposits or investments are backed by the full faith and credit of the United States. It would limit a receiver to only using fully-bonded bank accounts or Treasury securities. ICS bank accounts are FDIC-insured and currently offer interest rates up to 0.75% higher than those of funds held in bonded bank accounts because there is no requirement to purchase a surety bond.

Best Practices

Prior to making decisions about how and where to hold funds, a receiver should consult a banker about the estate’s needs and the safety of the institutions being considered, including financial information demonstrating the bank’s safety and soundness. The spectacular failure in 2023 of Silicon Valley Bank brought the credit risks of banks and the importance of ensuring that funds are fully protected into sharper focus. It would also be prudent to speak with the enforcement agency in the case if the appointment order directs or permits such communications, and to consider a conference with the judge if appropriate.

A receiver should also periodically provide copies of monthly statements to the enforcement agencies and courts to keep them and creditors apprised, and should obtain independent reviews of the bank, including from leading banking agencies, such as Bauer, S&P Global, Raymond James or others.

In summary, regardless of how receivership funds are invested, a receiver should take great care in determining how to hold and invest funds, and be able to demonstrate that several options have been considered given the specifics of the appointment order and the circumstances of the particular receivership.