A Fiduciary's Guide to Investment Strategies

By Freddie Smithson, CFA, CPA, CIRA

Attribution: This article draws upon research and analysis from 'A Receiver's Guide to Investment Strategies' by Freddie Smithson, published in The Receiver (Issue 18, August 2024), and 'Are Trustees Obligated to Invest in Interest-Bearing Accounts?' by Joseph E. Sarachek, Freddie Smithson, and Sarah Marlowe, published in the American Bankruptcy Trustee Journal (Volume 39, Issue 03).

Fiduciaries, whether serving as trustees in bankruptcy or court-appointed receivers, act as the financial stewards of an estate. This role carries a strict duty of care: to preserve assets, maintain liquidity, and--where prudent--generate yield for creditors and beneficiaries.

This responsibility is often complex. When distributions to claimants are expected to take months or years, the "opportunity cost" of leaving large balances in non-interest-bearing accounts becomes significant. However, the quest for yield must never compromise the safety of the principal.

The Golden Rule of Fiduciary Investing

Safety First, Liquidity Second, Yield Third.

Fiduciaries must weigh the potential for higher yields against the strict need for sufficient liquidity to cover immediate estate expenses and the absolute safety of the funds entrusted to them.

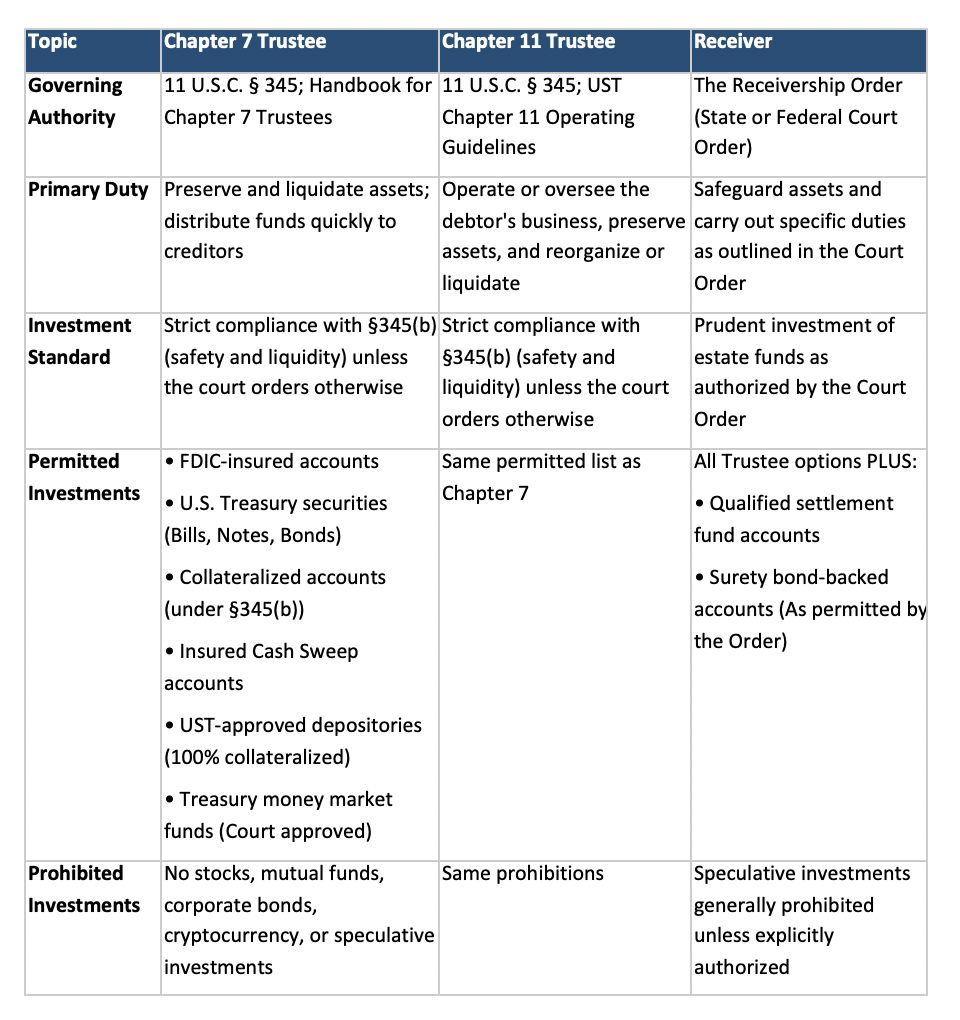

1. Comparative Guide: Trustee vs. Receiver

The following table outlines the governing authorities, duties, and investment standards for fiduciaries. While trustees are strictly governed by the Bankruptcy Code (specifically 11 U.S.C. § 345), receivers operate primarily under the specific authority of the court order appointing them.

2. Strategic Implementation: From Theory to Practice

Knowing what you are allowed to invest in is only the first step. Implementing a strategy requires assessing the lifecycle of the estate.

Phase 1: Immediate Liquidity (Months 0-6)

In the early stages of a case, liquidity is paramount. Unexpected expenses (insurance, legal fees, emergency repairs) are common.

Recommended Strategy: Keep funds in Authorized Depository checking accounts or Insured Cash Sweep (ICS) accounts.

Why: These provide instant access to cash while ensuring every dollar is insured or collateralized.

Phase 2: Stabilization (Months 6-18)

Once the initial chaos settles and you have a timeline for claims administration, you can segregate 'core cash' (needed for operations) from 'strategic cash' (held for distribution).

Recommended Strategy: Laddered U.S. Treasury Bills(T-Bills).

Why: Buying T-Bills with rolling maturities (e.g.,3-month, 6-month, and 12-month) allows you to capture higher yields than a standard savings account while ensuring portions of your cash mature regularly to cover expenses.

3. Risk Management & Compliance Checklist

For bankruptcy trustees, compliance with Section 345(b) is non-negotiable. For receivers, while you have more flexibility, adhering to these same standards acts as a 'safe harbor' against liability.

The 'Authorized Depository' Test

Before opening an account, ask the bank these three questions. If the answer to any is 'No,' do not deposit estate funds there.

1. Are you an authorized depository in this judicial district?

Note: Being authorized in one district does not automatically grant authority in another.

2. Do you have a Uniform Depository Agreement (UDA) on file with the U.S. Trustee?

Note: This agreement forces the bank to comply with collateral requirements.

3. Can you collateralize deposits that exceed the FDIC limit ($250,000)?

Note: If you deposit $1 million, the first $250k is covered by FDIC. The remaining $750k must be secured by the bank pledging stable securities (like Treasuries) equal to roughly 115% of the excess.

Documentation & Record Keeping

Fiduciaries are judged by their records. Maintain a distinct 'Investment Binder' (digital or physical) containing:

● Monthly Operating Reports (MORs): Clearly showing interest earned

● Trade Confirmations: For every purchase/sale of a Treasury security

● Collateral Reports: Monthly statements from the bank confirming they have pledged securities against your excess cash

● The Court Order: A copy of the specific order authorizing any investment outside the standard §345 list

4. Conclusion

The goal of a fiduciary is not to beat the market; it is to protect the estate. By adhering to the guidelines in 11 U.S.C. § 345 and establishing strict protocols for bank selection and collateralization, trustees and receivers can shield themselves from liability while maximizing the value available for creditors. When in doubt, prioritize safety over yield, and always seek court approval for any strategy that deviates from the standard path.